Findings from a survey of leading firms on labour market trends and the adoption of generative AI

Findings from a survey of leading firms on labour market trends and the adoption of generative AI

Agostino Consolo, Guzman Gonzalez-Torres Fernandez, Richard Morris and Christofer Schroeder

A recent ECB survey asked leading non-financial companies about the drivers of some key characteristics of the euro area labour market in recent years. These characteristics include an increased tendency for firms to cite recruitment difficulties; high and growing employment despite stagnating economic activity (and hence reduced labour productivity); a notable fall in average hours worked; and an increase in remote working. This part of the survey included a set of general statements with which respondents could agree, agree strongly, disagree, disagree strongly, or neither agree nor disagree. Respondents were asked to take a medium-term perspective, comparing the current environment with that of five to ten years ago. If they agreed or strongly agreed with a general statement, they were also asked to reply to a set of sub-statements exploring the reasons why.

The firms were also asked about the take-up of generative artificial intelligence (generative AI). Generative AI is the latest advancement in a phase of rapid technological development and has the potential to have a profound impact on the labour market and on productivity. The survey asked the firms: (i) whether they used generative AI operationally; and, if so, (ii) since when; (iii) what share of employees used generative AI for work at least once a week; and (iv) what were the main motivations for its adoption. The survey was sent to companies with which the ECB maintains regular contacts to gather information about the outlook for activity, prices and employment.[1] It ran from late May to end-June 2024 and received 46 responses.

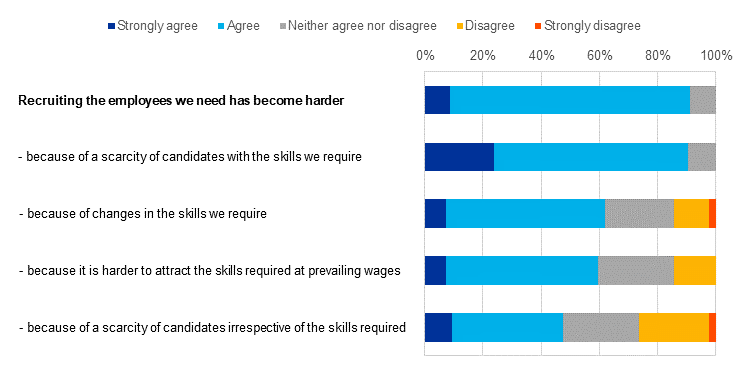

Respondents overwhelmingly agreed that recruitment had become harder in recent years, emphasising a scarcity of workers with the required skills (Chart A). More than 90% agreed or strongly agreed with the statement that recruiting the employees they needed had become harder than five to ten years ago, which is indicative of widespread labour shortages. Of these, 90% agreed that there was a scarcity of candidates with the skills they required, suggesting shortages of skilled labour. A somewhat smaller – albeit significant – share (slightly below 50%) said that there was a general scarcity of candidates, irrespective of the skills needed. Firms seeing a general scarcity of candidates were mostly those active in labour-intensive service industries or with significant production in Germany. As regards demand factors, around two-thirds agreed that changes in the skills they asked for had led to increased hiring difficulties, while almost 60% said that prevailing wage rates made it harder to attract employees with the necessary skills.

Chart A

Summary of responses in relation to labour shortages

(percentages of responses)

Source: ECB.

Notes: Bars indicate the percentages of respondents that gave each of the five possible responses. All respondents were asked to reply to the general statement in bold. If they agreed or strongly agreed, they were also asked to respond to the sub-statements. Shares for the sub-statements refer to the subset of respondents that agreed or strongly agreed with the general statement.

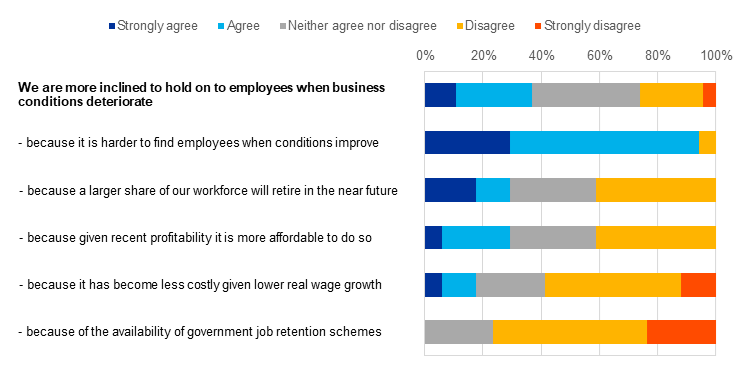

Slightly more than a third of the respondents agreed that their firms were more inclined to retain employees when business conditions deteriorated, with almost all linking this to the anticipated difficulty of recruiting when conditions improved (Chart B). This points to a strong link between labour hoarding and labour shortages. There was more disagreement than agreement with each of the other sub-statements, although around half of the firms that were more inclined to retain staff did agree that at least one other factor was relevant. Around one-third said that an expected increase in retirements in the near future was a factor. A similar share agreed that recent profitability had made holding on to labour more affordable, and around 20% agreed that lower real wage growth was a motivation. This lends some, albeit limited, support to earlier analyses of the importance of these factors for the resilience of employment since the end of 2022.[2] No respondents agreed with the statement that government job retention schemes were a contributing factor.

Chart B

Summary of responses in relation to labour hoarding

(percentages of responses)

Source: ECB.

Note: See the notes to Chart A.

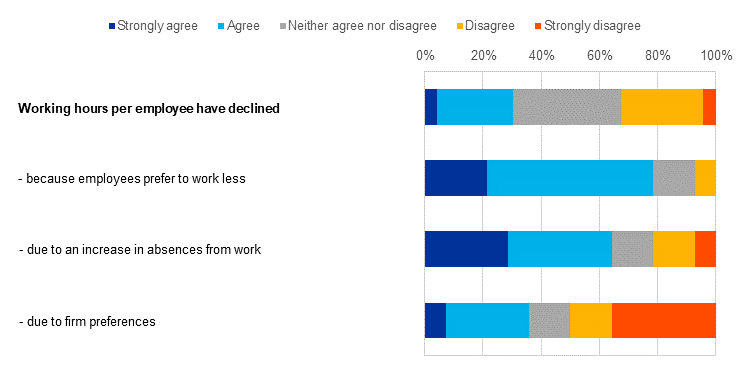

Among the respondents agreeing that working hours per employee had declined, the most important reason given was employees’ preference for working less (Chart C). 80% of those who agreed that working hours had declined said this was (at least in part) because employees preferred to work less, and two-thirds perceived an increase in absences from work as a factor. By contrast, only a third said it reflected the firm’s preferences (while more than half disagreed with this sub-statement, including one-third who strongly disagreed).

Chart C

Summary of responses in relation to hours worked

(percentages of responses)

Source: ECB.

Note: See the notes to Chart A.

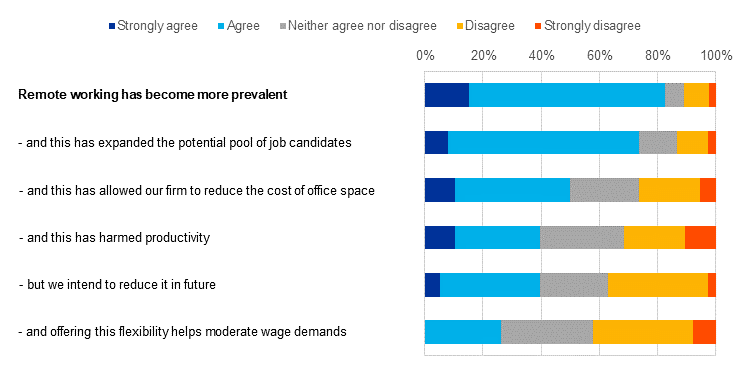

Respondents confirmed the widespread increase in remote working, with most agreeing that this expanded the potential pool of job candidates (Chart D). Of the slightly more than 80% who said remote working had become more prevalent, three-quarters agreed this had expanded the potential pool of job candidates. Around a half said it had allowed their firm to reduce office space and associated fixed costs. By contrast, only a quarter agreed that it had helped to moderate wage demands, whereas almost half disagreed. Around 40% agreed with the statement that the increase in remote working had harmed productivity (with a similar share saying they intended to reduce remote working in future), while just over 30% disagreed.

Chart D

Summary of responses in relation to remote working

(percentages of responses)

Source: ECB.

Note: See the notes to Chart A.

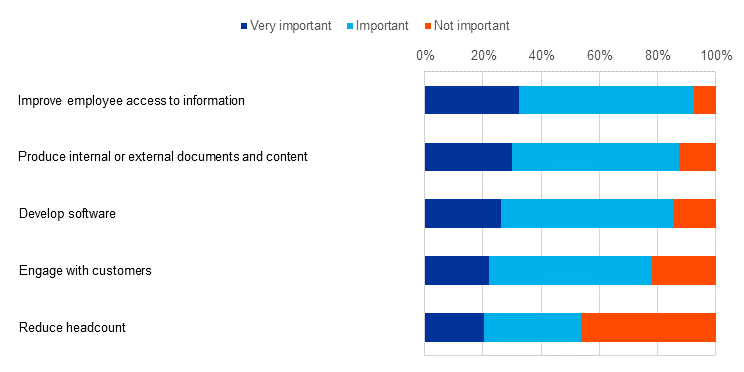

Turning to the questions on the use of generative AI, almost three-quarters of respondents said their firms were already using this technology, and the motivations for doing so were broad-based (Chart E). Among those already using generative AI operationally, most had started relatively recently, with a significant take-up during 2023. About half estimated that not more than 10% of their workforce used generative AI at least once a week, while only 6% put the share of their workforce regularly using the technology at above 25%. As regards the main motivations for adopting generative AI, improving employees’ access to information ranked first, being considered important or very important by more than 90% of respondents. This was very closely followed by the use of generative AI to produce content, develop software and engage with customers. Around half of those using the technology agreed that reducing headcount was also an important motivation. Additionally, several respondents emphasised that the use of generative AI was still in an experimental phase, with businesses learning and seeking to identify use cases to raise productivity, quality and efficiency.

Chart E

Summary of responses in relation to the main motivations for adopting generative AI

(percentages of responses)

Source: ECB.

Note: Bars indicate the percentages of respondents that gave each of the three possible responses.

-

For further information on the nature and purpose of these contacts, see the article entitled “The ECB’s dialogue with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2021.

-

See the boxes entitled “Higher profit margins have helped firms hoard labour” and “Drivers of employment growth in the euro area after the pandemic – a model-based perspective”, Economic Bulletin, Issue 4, ECB, 2024.

Poslední zprávy z rubriky Makroekonomika:

Přečtěte si také:

Příbuzné stránky

- Alkohol - kalkulačka on-line

- Statement of the Ministry of Foreign Affairs of the Czech Republic on the Russian invasion against Ukraine

- Implementation of sanctions: additional guidance on the transit of goods from Russia

- Key findings of the 2022 Report on Bosnia and Herzegovina

- Hearing of the Committee on Economic and Monetary Affairs of the European Parliament - Christine Lagarde

- Czech National Bank Survey on Macroprudential and Monetary Policy: Summary of the Results

- The Czech labour market is currently starting to be dominated by wages catching up with the increased price level - The development of the Czech labour market - 2. quarter of 2023

- The head of Czech diplomacy visited the attacked Israel, from which he evacuated dozens of Czechs

- Election to the Senate of the Parliament of the Czech Republic held on 5.10. – 6.10.2018

Prezentace

12.02.2025 iPhone 16 Pro za 699 Kč! Nová služba nemá v…

29.01.2025 Xiaomi má nový bestseller. Je extrémně nadupaný a

28.01.2025 České firmy stále častěji místo banky…