Bank of Russia’s decisions on macroprudential requirements for unsecured consumer loans (29.11.2024)

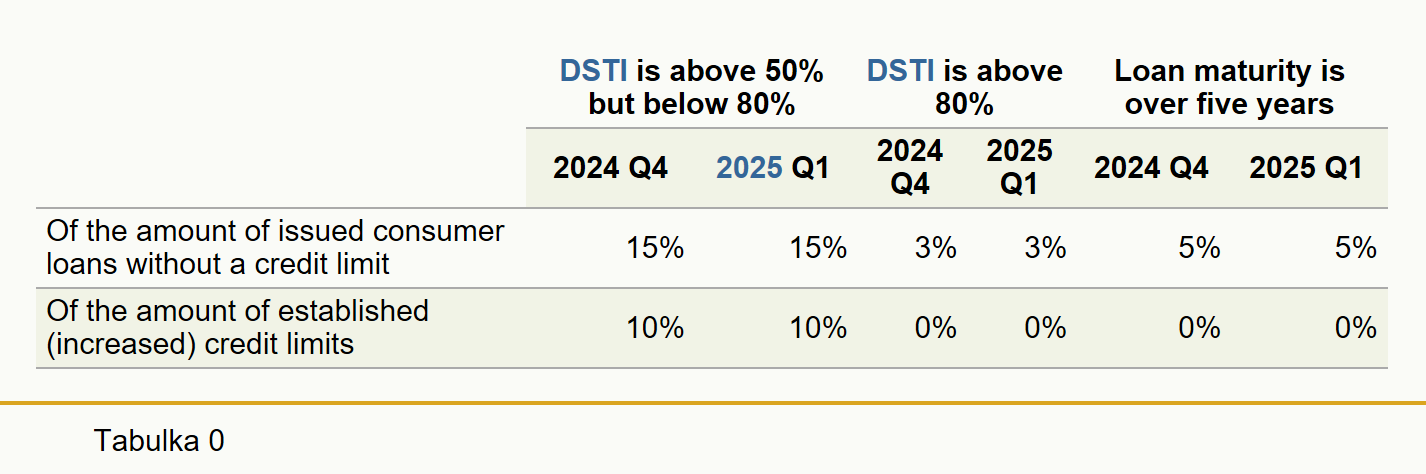

The Bank of Russia has decided to retain the parameters of macroprudential limits (MPLs) on unsecured loans for 2025 Q1 the same as those set for 2024 Q4 (Tables 1 and 2).

Furthermore, the Bank of Russia has reduced the risk-weight add-ons for unsecured consumer loans (Table 3).

The expansion of the unsecured consumer loan portfolio slowed down as a result of tight monetary policy and countercyclical macroprudential policy. Specifically, the monthly growth rate of the portfolio decreased from 2% in May—June 2024 to 1.3–1.4% in July—August 2024, equalling 0.7% in September 2024 and turning negative (-0.3%) in October 2024. The most significant deceleration was in the segment of cash loans: outstanding cash loans were up by 0.5%1 over 2024 Q3, compared with 4.7% in 2024 Q2. Contrastingly, the debt on credit cards continued to grow rapidly, namely by 12% in 2024 Q3 vs 9% in 2024 Q2. The increase was largely because individuals started to more actively use the limits on earlier issued credit cards.

The effective MPLs improve the lending standards: the proportion of unsecured consumer loans issued to borrowers with debt service-to-income ratios (DSTI) exceed 50% contracted from 63% in 2022 Q4 to 28%2 in 2024 Q3, with the share of these loans in the portfolio declining from 64% to 49%. Furthermore, the leading indicators (the percentage of loans overdue for 30 days after the first three months on book) show that the quality of loans stabilised after a slight worsening in early 2024.

Maintaining the current MPLs values for 2025 Q1 will help further shift towards a more balanced structure of the portfolio of outstanding consumer loans, prevent an increase in households’ debt burden, reduce banks’ and microfinance organisations’ risks, and ultimately, enhance financial stability.

After the approval of the matrix of the add-ons effective from 1 September 2024 (the press release, dated 28 June 2024), the key rate was raised by five percentage points. Amid growing interest rates, banks are increasing effective interest rates (EIRs) for borrowers with the same credit risk level because of higher funding costs. In view of this, the matrix of the add-ons differentiated by EIR levels is becoming tighter.

To enable banks to issue loans amid higher interest rates without increasing the burden on their capital, the Bank of Russia has decided to adjust the matrix of the risk-weight add-ons from 2 December 2024.

Table 1. MPLs for banks (except for banks with a basic licence)

| DSTI is above 50% but below 80% | DSTI is above 80% | Loan maturity is over five years | ||||

|---|---|---|---|---|---|---|

| 2024 Q4 | 2025 Q1 | 2024 Q4 | 2025 Q1 | 2024 Q4 | 2025 Q1 | |

| Of the amount of issued consumer loans without a credit limit | 15% | 15% | 3% | 3% | 5% | 5% |

| Of the amount of established (increased) credit limits | 10% | 10% | 0% | 0% | 0% | 0% |

Table 2. MPLs for microfinance organisations

| DSTI is above 50% but below 80% | DSTI is above 80% | Loan maturity is over five years | ||||

|---|---|---|---|---|---|---|

| 2024 Q4 | 2025 Q1 | 2024 Q4 | 2025 Q1 | 2024 Q4 | 2025 Q1 | |

| Of the amount of issued consumer loans without a credit limit | 15% | 15% | 3% | 3% | No limit | |

| Of the amount of established (increased) credit limits | 10% | 10% | 0% | 0% | No limit | |

Table 3. Risk-weight add-ons for unsecured consumer loans issued beginning on 2 December 2024

| Add-on | Borrowers’ DSTI, % | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| W/o DSTI | (0–30] | (30–40] | (40–50] | (50–60] | (60–70] | (70–80] | (80+)4 | ||

| EIR, % p.a. | (0–10] | 1.8 | 0.0 | 0.0 | 0.2 | 0.3 | 0.7 | 1.2 | 1.8 |

| (10–15] | 2.0 | 0.0 | 0.2 | 0.3 | 0.5 | 0.9 | 1.4 | 2.0 | |

| (15–20] | 2.4 | 0.4 | 0.5 | 0.7 | 0.9 | 1.3 | 1.8 | 2.4 | |

| (20–25] | 2.9 | 1.0 | 1.2 | 1.4 | 1.7 | 2.0 | 2.3 | 2.9 | |

| (25–30] | 3.6 | 1.6 | 1.7 | 1.9 | 2.2 | 2.6 | 3.0 | 3.6 | |

| (30–40] | 3.8 | 1.7 | 1.8 | 2.0 | 2.6 | 3.0 | 3.2 | 3.8 | |

| (40–50] | 4.0 | 1.8 | 2.0 | 2.2 | 3.0 | 3.2 | 3.5 | 4.0 | |

| (50–60] | 5.0 | 2.0 | 2.2 | 2.5 | 3.2 | 3.5 | 4.0 | 5.0 | |

| (60+) | 6.0 | 6.0 | 6.0 | 6.0 | 6.0 | 6.0 | 6.0 | 6.0 | |

1 According to Reporting Form 0409704.

2 For credit cards and cash loans, the data are based on Reporting Forms 0409704 and 0409135, respectively.

3 The percentage of loans actually issued to borrowers with DSTI above 50% exceeds the amount of the MPLs set for 2024 Q3 on loans to borrowers with DSTI of 50–80% and DSTI over 80% because a part of the outstanding debt is that on credit cards issued before the tightening of the MPLs or even before their establishment (the MPLs on credit cards restrict the proportion of the limits newly opened or increased by creditors and not the proportion of earlier issued loans to borrowers with high DSTI since the decision on using the limit is made by borrowers).

4 Including on loans for which the calculation of DSTI was not mandatory.

{kind=link}

{kind=link}

{kind=link}