Consumer risk-taking and stock market investment: Insights using the CES’s consumer finance module

- 27 MAY 2024 · RESEARCH BULLETIN NO. 119

Consumer risk-taking and stock market investment: Insights using the CES’s consumer finance module

by Dimitris Christelis, Dimitris Georgarakos, Tullio Jappelli and Geoff Kenny[1]

Investing in the stock market is seen to have numerous potential benefits for households, including: possible higher returns on investment; lower risk through more diversification; and some protection against inflation. These advantages are potentially important for long-term financial well-being and retirement planning. However, there may be excessive barriers to households investing in stocks, which may prevent people from reaping these potential rewards. In addition, households’ willingness to invest in the stock market can be revealing about their attitudes to financial risk-taking. Understanding these preferences is critically important when building models of the business cycle, in order to accurately capture the transmission of financial shocks.

In our recent study (Christelis, Georgarakos, Jappelli and Kenny, 2024) we aim to shed light on these issues. In particular, we investigated whether a sudden increase in wealth has an impact on how much money – if any – a household is willing to invest in the stock market. We aim to identify the causal effect of increases in household wealth on stockholding. This is not an easy task: stock market investment can also be a primary cause of increases in wealth, resulting in a “chicken or egg” problem.[2]

Unexpected wealth increases and stock market participation

In order to better understand this relationship between wealth and stock market investment, we conducted an experiment using the ECB’s Consumer Expectations Survey (CES).[3] In our experiment, we invited participants in the June 2021 CES to imagine that they had won a lottery prize and asked them how they would use this unexpected increase in wealth over the next 12 months.[4] They were given three options: they could either use the hypothetical prize money to buy goods and services, repay debts, or save it and invest in financial assets. We randomly assigned participants five different lottery prizes (€5,000, €10,000, €20,000, €30,000 and €50,000) to also assess whether the size of the win would affect their decisions.

On average, our results show that 34% of the unexpected increase in wealth is used for consumption, 18% is used to repay debt, while the remaining 48% is saved and invested. We then asked those who indicated that they would use the winnings to save and invest in financial assets how much they would allocate to different investment categories. In practice, consumers can invest in stocks either directly or indirectly by purchasing shares in a stock mutual fund.[5] By focusing on the amounts allocated to these two investment options, we were then able to trace how changes in wealth affect stock market behaviour. With nearly 10,000 respondents to the CES, our results cover a representative cross-section of the euro area population.

To enrich this experimental evidence, our study also drew on information about the households’ actual financial assets and liabilities. This information is typically collected once a year as part of a new consumer finance module in the CES. On the asset side it gathers information on financial wealth, including various investments, cash holdings and bank deposits. On the liability side the data cover loans, such as car loans, mortgages or student loans. This information can then be linked with other CES information collected at a higher frequency, e.g. every month.[6]

Would consumers buy stocks if their wealth increased by €50,000?

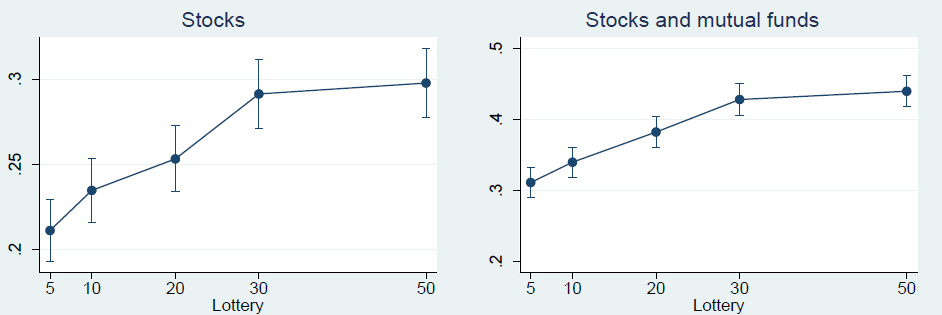

The first question we address is how changes in consumers’ wealth can influence the decision on whether or not to hold stocks at all. The answer to this question is particularly insightful in helping to understand the barriers to stock market participation. We found that increases in wealth do encourage some households to invest in stocks. The share of respondents willing to invest in stocks or stocks and mutual funds increases with the size of the hypothetical lottery gain (see Chart 1). In more formal modelling, we show that there is a 6.3 percentage point (pp.) increase in stock market participation when comparing the largest with the smallest lottery gain, and a 12.8 pp. rise when considering stocks and mutual funds combined. We also found that the probability of investing in the stock market is linked to the size of the wealth increase. Those receiving a bigger hypothetical windfall, e.g. above €20,000, were more likely to invest in stocks.

Chart 1

Proportion of households investing in stocks by lottery prize

Share of CES respondents

Sources: ECB Consumer Expectations Survey and Christelis, Georgarakos, Jappelli and Kenny (2024).

Notes: The wealth shock is derived from a hypothetical windfall lottery gain that is randomly distributed across CES respondents. There are five different windfall gain amounts of €5,000, €10,000, €20,000, €30,000 and €50,000. The sample used comprises all CES respondents to our survey experiment. The y-axis depicts the proportion of survey respondents that intend to invest in stocks and the associated 95% confidence bands. Averages are computed using sample weights.

Overall, however, a key finding is that, regardless of the change in consumers’ wealth, the effect on stock market participation is limited. Even after a windfall of €50,000, a majority of respondents would still not invest in stocks or mutual funds at all! Such a large increase in wealth should easily absorb not only all relevant transaction costs, but also the “entry” costs of buying stocks for the first time, such as setting up a new custody account. This strongly suggests that entry costs are only partly responsible for limited stock market participation by households. Rather, consumers may hold negative beliefs about stock markets (e.g. related to the perceived risks) or lack trust in financial institutions. On top of this, “inertial behavior”, or the tendency to avoid change, and other biases are also likely to weigh on consumers’ decisions. Finally there may be significant information-processing costs, such as the time needed to understand stock markets, make decisions about which stocks to hold and how to buy them, that deter stock market investment.

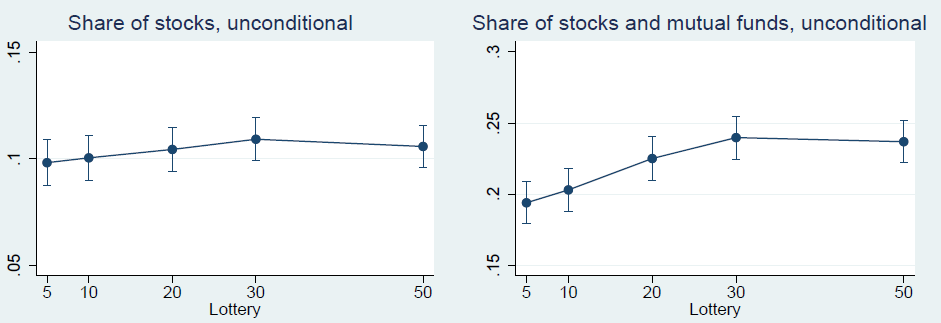

Chart 2

Share of financial wealth invested in stocks by lottery prize

Share of total amount saved that is invested in stocks or stocks and mutual funds

Sources: ECB Consumer Expectations Survey and Christelis, Georgarakos, Jappelli and Kenny (2024).

Notes: The wealth shock is derived from a hypothetical windfall lottery gain that is randomly distributed across CES respondents. There are five different windfall gain amounts of €5,000, €10,000, €20,000, €30,000 and €50,000. The sample used comprises all CES respondents to our survey experiment (i.e. unconditional on stock market participation). The y-axis depicts the asset share together with 95% confidence bands. The asset share is computed as the ratio of the amount invested in stocks (or stocks and mutual funds) over the total amount that survey respondents indicated that they would save. Averages are computed using sample weights.

Do households take proportionately more risk as overall wealth rises?

The second question we answer is how changes in wealth can influence the share of a consumer’s total portfolio they are willing to allocate to stocks and shares. This speaks more directly to the nature of consumers’ risk aversion.[7] Results from our experiment suggest that the share invested in stocks is relatively constant at about 11% when considering all CES respondents (see left-hand panel of Chart 2). This finding points to relatively constant risk aversion. However, when we consider the combination of stocks and mutual funds, the share appears to increase somewhat.

In exploring this question further, it is particularly useful to focus on those respondents who, according to their actual financial situation as typically reported in the CES’s consumer finance module, have already invested in stocks. For this subset of respondents, we find that the share invested in stocks (or stocks and mutual funds) remains fairly constant regardless of the size of the wealth shock. Looking in more detail at our results, we can compare the share of overall financial wealth invested in stocks or stocks and mutual funds for a hypothetical prize of €50,000 and one of €5,000. The larger prize increases the share by 1.7 percentage points more. This suggests that for larger changes in wealth, risk aversion may decrease slightly.[8] Finally we also found some modest differences in the response of the asset share depending on the consumer’s access to liquidity. Households with greater access to liquidity tend to increase their asset share proportionately more compared with households that have liquidity constraints. [9] In contrast, no significant differences were identified related to respondents’ level of financial literacy, how trusting they are of others or their level of perceived household income risk.

Conclusions

We found that households are generally reluctant to invest in stocks, and this remains the case even when they experience a relatively large increase in wealth. This demonstrates the effect of barriers to stock market participation, such as a lack of trust and other behavioural biases that may shape beliefs about stock prices. Our results are also consistent with the idea that risk aversion remains relatively constant even with an unexpected change in wealth. This would support the assumptions commonly used in many macroeconomic models. However, it may nevertheless be useful to consider building more variation into households’ risk preferences when trying to model the business cycle and, in particular, the transmission of financial shocks.

References

Andersen, S. and Nielsen, K. M. (2011), “Participation Constraints in the Stock Market: Evidence from Unexpected Inheritance Due to Sudden Death”, The Review of Financial Studies, Vol. 24, No 5, pp. 1667-1697.

Briggs, J., Cesarini, D., Lindqvist, E. and Östling, R. (2021), “Windfall gains and stock market participation”, Journal of Financial Economics, Vol. 139, Issue 1, pp. 57-83.

Calvet, L. E. and Sodini, P. (2014), “Twin Picks: Disentangling the Determinants of Risk-Taking in Household Portfolios”, The Journal of Finance, Vol. 69, No. 2, pp. 867-906.

Christelis, D., Georgarakos, D., Jappelli, T. and Kenny, G. (2024) “Wealth shocks and portfolio choice”, forthcoming, ECB Working Paper series.

European Central Bank (2021), “ECB Consumer Expectations Survey: an overview and first evaluation”, Occasional Paper Series, No. 287, December.

Georgarakos, D. and Kenny, G. (2022), “Household spending and fiscal support during the COVID-19 pandemic: Insights from a new consumer survey”, Journal of Monetary Economics, Vol. 129, pp. S1-S14.

Stantcheva, S. (2023), “How to Run Surveys: A Guide to Creating Your Own Identifying Variation and Revealing the Invisible”, Annual Review of Economics, Vol. 15, pp. 205-234.

-

This article was written by Dimitris Christelis (University of Glasgow), Dimitris Georgarakos (Directorate General Research, European Central Bank), Tullio Jappelli (University of Naples Federico II) and Geoff Kenny (Directorate General Research, European Central Bank). The authors gratefully acknowledge the comments of Alex Popov, Mark Hughes and Zoë Sprokel. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank or the Eurosystem.

-

Previous studies in this field have measured the effect of wealth increases on stockholding after particular events, such as inheriting in Denmark (Andersen and Nielsen, 2011) and winning a lottery prize in Sweden (Briggs et al., 2021). However, such studies may still not tell the full story as they refer to specific segments of society.

-

As described in ECB (2021) and Georgarakos and Kenny (2022), the CES is an online panel survey that is currently conducted on a monthly basis across 11 euro area countries. The CES was developed in 2020 and is a highly representative survey of the euro area population. Further information is also available via the CES webpage.

-

Stantcheva (2023) provides examples in which this scenario approach using hypothetical questions can shed light on a variety of different fields, including education, labour, health, and macro-finance.

-

The full set of options were: (i) current and saving accounts; (ii) stocks and shares; (iii) mutual funds; (iv) retirement and pension products (including life insurance); and (v) bonds.

-

The case for collecting this balance sheet information once a year is supported by existing research which has documented that households exhibit considerable inertia in rebalancing their portfolios. This implies that the structure of households’ “balance sheets” changes relatively slowly over time. Moreover, the detailed questions about financial assets and liabilities cannot be repeated frequently, as they add considerably to the effort required from survey respondents.

-

For example, if the level of risk aversion remains the same even as wealth increases, consumers may tend to keep the proportion of their total portfolio allocated to stocks and shares relatively constant. Alternatively, if they become less risk averse as their wealth increases, they might tend to hold a higher share in stocks.

-

In an earlier study using Swedish data on the financial portfolios of twins, Calvet and Sodini (2014) report evidence that the asset share increases with financial wealth, lending support to the notion of decreasing risk aversion.

-

In our framework, liquid consumers indicate in a separate question that they have sufficient financial resources to be able to make an unexpected payment equal to one month of their household’s income, while illiquid households indicate that they do not have the ability to make such a payment.