The dynamics of inflation differentials in the euro area

Prepared by Anastasia Allayioti and Anna Beschin

Published as part of the ECB Economic Bulletin, Issue 5/2024.

The surge in euro area inflation in 2021 and 2022 came with a sizeable increase in inflation dispersion across countries. Persistent inflation divergences across euro area countries can have implications for the transmission of the single monetary policy. The ECB therefore monitors developments in, as well as the nature of, inflation differentials. This box explores this issue with a focus on the recent inflation surge.

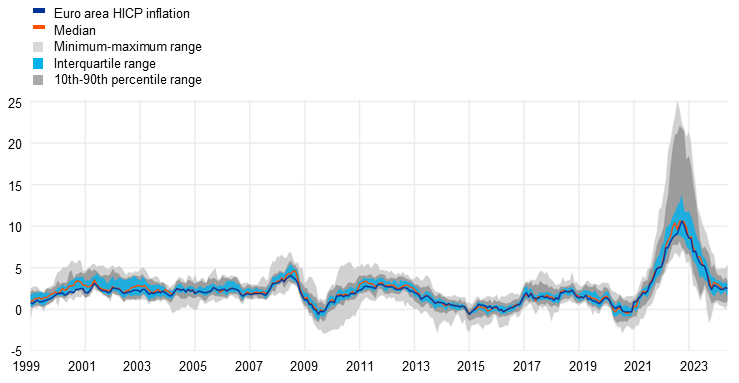

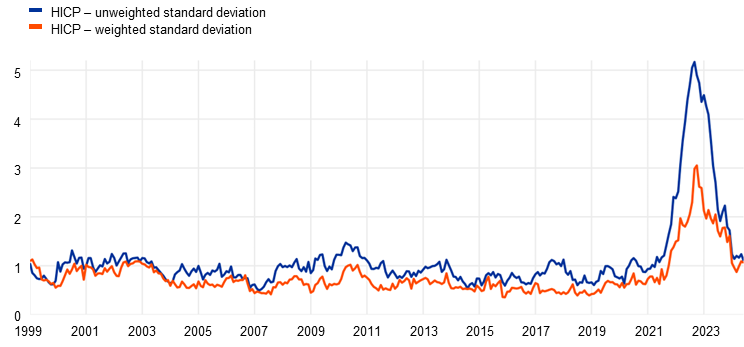

Most of the dispersion in headline inflation rates following the pandemic and Russia’s invasion of Ukraine has unwound. Following the low and even negative inflation rates recorded during the pandemic, inflation started to rebound in 2021 and differentials across euro area countries began to increase (Chart A).[1] By the end of 2022 differentials had risen to historical highs, exceeding the peaks observed during the 2007-2008 global financial crisis. When headline inflation peaked at 10.6% in October 2022, inflation rates ranged from 7.1% in France to 22.5% in Estonia. Much of the dispersion measured in terms of standard deviations was accounted for by smaller euro area countries and, in particular, the Baltic States. Scaling the standard deviation outcomes with the relative weights of the countries in the Harmonised Index of Consumer Prices (HICP) (see the red line in Chart A, panel b) reduces the measured dispersion but also highlights how historically exceptional these recent shifts were. Developments between the end of 2022 and June 2024 imply a strong and almost symmetric reversal of dispersion, although some recent fluctuation has taken it slightly above pre-pandemic levels. The overall strong reversal implies that this dispersion pattern is temporary rather than persistent in nature. Moreover, the reversal shows that the sharpest declines in inflation rates were recorded in those countries that had previously seen the strongest surges.

Chart A

Headline inflation differentials

a) HICP inflation range

(annual percentage changes)

b) HICP standard deviations

(standard deviations)

Sources: Eurostat and ECB staff calculations.

Notes: The latest observations are for June 2024. In panel b), the weighted standard deviation is computed by considering the country weights (household final monetary consumption expenditure) within the euro area.

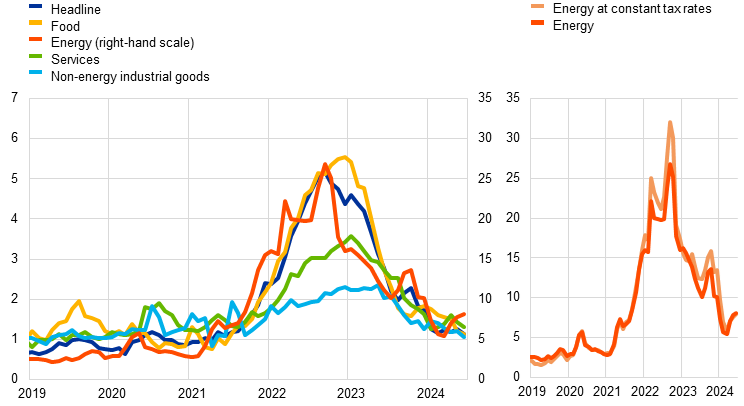

Energy and food prices played a significant role in this recent dispersion of headline inflation rates. The pandemic and the war in Ukraine gave rise to a unique combination of common shocks affecting euro area countries. Inflation surged owing to supply bottlenecks, post-pandemic reopening effects and large increases in energy and food commodity prices. While the types of shock were common to all euro area countries, the subsequent dispersion in national headline inflation rates implies varying degrees of exposure to and different economic impacts stemming from those shocks. The dispersion is driven by differences in economic structures, adjustment mechanisms and policy responses. For instance, countries that have a higher share of energy and food in the HICP basket are, in principle, more strongly affected by a common shock in the underlying commodity prices. Differences in energy and food inflation therefore account for most of the headline inflation dispersion (Chart B, panel a). In the case of energy inflation, this was partly due to differences in countries’ energy mixes (for example in fuels, gas and electricity, which contribute the most to HICP energy), contract and consumption patterns, regulatory approaches and government support measures.[2] The dispersion of energy inflation rates around the inflation peak is higher when calculated on the basis of the HICP energy at constant tax rates (Chart B, panel b), indicating a moderating impact of government measures.[3] Dispersion in food inflation peaked later than dispersion in energy inflation, but has since declined substantially, also reflecting, as in the case of energy, the downward trend in global commodities prices since mid-2022.

Chart B

Dispersion of headline inflation and its components across euro area countries

(standard deviations)

Sources: Eurostat and ECB staff calculations.

Note: The latest observations are for June 2024.

The dispersion of the subcomponents of core inflation (goods and services) has also been sizeable across countries (Chart B, panel a). Different speeds of reopening and different exposures to supply disruptions following the pandemic are likely to have been behind these divergences. Heterogeneous indirect effects from high energy costs may have been another factor. Dispersion in non-energy industrial goods inflation has been consistently the lowest among all HICP subcomponents since mid-2021. This may be because this subcomponent reflects the prices of internationally traded goods such that the determinants of the dispersion are more homogeneous across countries. By comparison, dispersion in services inflation was visibly higher. It is likely that this reflects differing developments in many services items, such as travel, rent and some administered prices, owing, for example, to heterogeneous indirect effects from energy or food prices, and different weights across countries. By June 2024 dispersion had fallen back to pre-pandemic levels for both non-energy industrial goods inflation and services inflation. While for goods this implies more alignment around historical average levels of inflation, in the case of services it means alignment around a still elevated level. A reduction in the dispersion would therefore be compatible with the notion that, across countries, common factors are driving the persistence of services inflation.

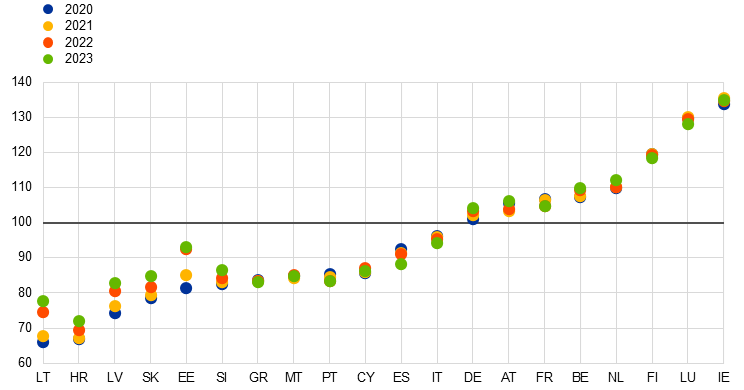

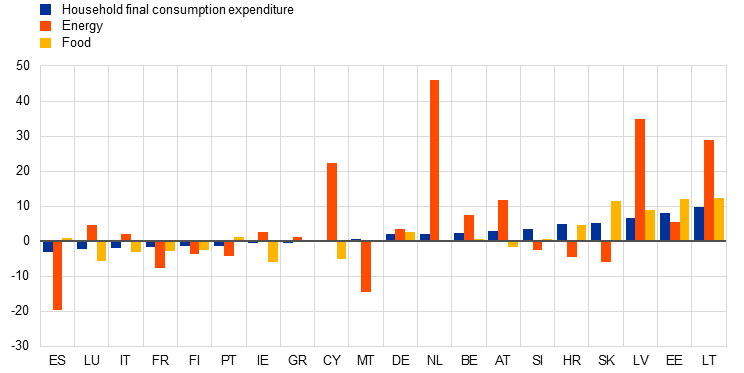

Elevated inflation differentials during the surge in inflation did not by and large result in substantial changes in the overall relative price levels between countries. While the surge in inflation and its unwinding in recent years have not had a lasting impact on inflation differentials, this does not rule out more persistent implications for relative national price levels and living costs and, ultimately, for the relative competitiveness of some countries vis-a-vis their euro area peers. An important indicator for this type of assessment is the price level index (PLI) published by Eurostat.[4] Focusing on the years since 2020 and the large swings in inflation recorded, it appears that the surge in inflation has not led to substantial changes in relative price levels for most countries (Chart C). However, considerable increases are observed for some of the smaller countries, such as the Baltic States between 2021 and 2023, when the cost of living saw an upward adjustment relative to the euro area-wide price level. This upward adjustment edged up somewhat further in 2023, although inflation dispersion was already decreasing. Upward adjustments, albeit of smaller scale, are also observed for the other central and eastern European (CEE) countries, Croatia, Slovenia and Slovakia.[5] Among the larger euro area countries, inflation developments hardly had any impact on the relative price level, which rose slightly in the case of Germany and the Netherlands but declined somewhat for Spain, France and Italy. In many countries, energy and food had the opposite effect on the movement of the overall relative price level between 2021 and 2023, but for the Baltic States both components operated in the same upside direction (Chart D). In the case of France, energy and food both contributed to a decline in the relative overall price level compared with that of the euro area.

Chart C

Comparative price levels across the euro area

Household total consumption expenditure

(price level index; euro area = 100)

Source: Eurostat.

Note: Countries have been sorted in ascending order on the basis of their 2020 PLI.

Chart D

Changes in comparative price levels between 2021 and 2023 across the euro area

(point changes in price level index)

Summing up, euro area inflation differentials rose sharply in the aftermath of the pandemic and the energy crisis but have since largely returned to pre-pandemic levels. Cross-country differences in energy and food inflation were the main drivers of both the increase in and the recent reversal of overall inflation dispersion, reflecting the fact that the initial commodity price shock has, to a large extent, been absorbed. At the same time, it appears that the temporarily high dispersion of inflation across countries will, for some of the smaller euro area countries, have more persistent implications in terms of an upward adjustment in their relative price levels.

-

Cross-country differentials for the years under examination are calculated on the basis of the euro area’s composition at a particular point in time.

-

The introduction and eventual withdrawal of energy and inflation compensatory fiscal measures has not been homogeneous across countries. Most recently, changes across the largest five euro area countries have included the expiry of VAT reductions on different energy components (Germany, Spain and Italy), the reversal of reductions in excise taxes and system charges (Spain, Italy and the Netherlands), the expiry of a cap on regulated gas price increases (Spain) and a decrease in the support measures for the electricity price shield (France).

-

The impact of indirect taxes likely understates the overall impact of government measures on differentials in energy inflation, as some measures took the form of subsidies to households or regulated prices (and also price caps).

-

PLIs are published with a lag. The latest available data are those for 2023, published in June 2024. For euro area countries (which share a common exchange rate), PLIs measure the difference in price levels between countries for the same (basket of) goods or services. The average is indexed to 100: if the PLI is higher than 100, the country concerned is relatively expensive compared with the euro area, but if the value of the index is below 100 the country is relatively cheap. For methodological information, see the web page on purchasing power parities on Eurostat’s website.

-

This considerable relative adjustment of price levels for the Baltic States and some other CEE countries is also visible in HICP data. Compared with 2019, their indices of headline HICP in 2023 were approximately 5-15% higher than the euro area aggregate index. On balance, data for the first half of 2024 broadly confirm the relative adjustment observed by 2023.