Europe’s tragedy of the horizon: the green transition and the role of the ECB (Piero Cipollone)

Speech by Piero Cipollone, Member of the Executive Board of the ECB, at the Festival dell’ Economia di Trento

Trento, 26 May 2024

It is a great pleasure to be here.

As we meet today, we find ourselves at a critical juncture. Faced with the severe negative effects of climate change, we have to act swiftly while seizing the economic opportunities that the green transition offers.

I would like to focus on three important aspects. I will first talk about the increasing costs of climate change and the considerable investments the green transition requires. I will then discuss the implications for central banks and the role that the ECB can play. And finally, I will outline how this role interacts with the actions of other policymakers across Europe when it comes to facing the challenges ahead.

The growing cost of climate change

Historically, efforts to combat climate change were often hampered by what Mark Carney defined as the “Tragedy of the Horizon”: the impact of climate change was typically felt to be beyond the time horizon of most economic actors and policymakers, thus diminishing their urgency to act.[1]

However, we have reached a turning point and we cannot afford to delay any further, as the situation is changing rapidly, especially for Europe.

Global temperatures are rising faster than ever. The warmest years on record have been concentrated in the past decade, with 2023 being particularly extreme.[2] The accelerating pace of climate change is associated with an increase in the frequency of wildfires, periods of drought, heatwaves, and hurricanes and storms, all of which have contributed to growing environmental degradation and biodiversity loss.[3]

Europe is particularly affected by these changes. The European State of the Climate report 2023 indicates that Europe is the fastest-warming continent in the world, warming at twice the global average rate since the 1980s.[4] From 1980 to 2022 weather and climate-related events resulted in economic losses totalling around €650 billion in the EU. Annual losses in 2022 were 41% higher than in 2009.[5]

This trend of rising temperatures and related damages is more problematic than ever. Our economies have not yet devised a way to properly allocate the risks of negative climate events to entities capable of dealing with them, as reflected in low insurance coverage. According to a joint report by the ECB and the European Insurance and Occupational Pensions Authority (EIOPA), only a quarter of losses from extreme weather and climate events in the EU are insured.[6] Insurance coverage is even lower among the less affluent parts of the population, who tend to own housing that is more exposed to natural catastrophe risks and who, in relation to their income levels, face a higher cost of protection.[7]

Although it is leading the transformation at global level, and despite the considerable efforts made so far, the EU is currently not yet on track to meet its climate targets for 2030 and 2050.[8] Further action is needed.

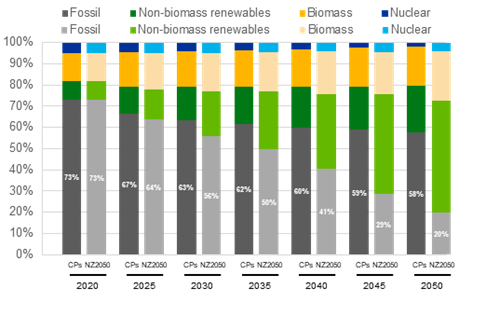

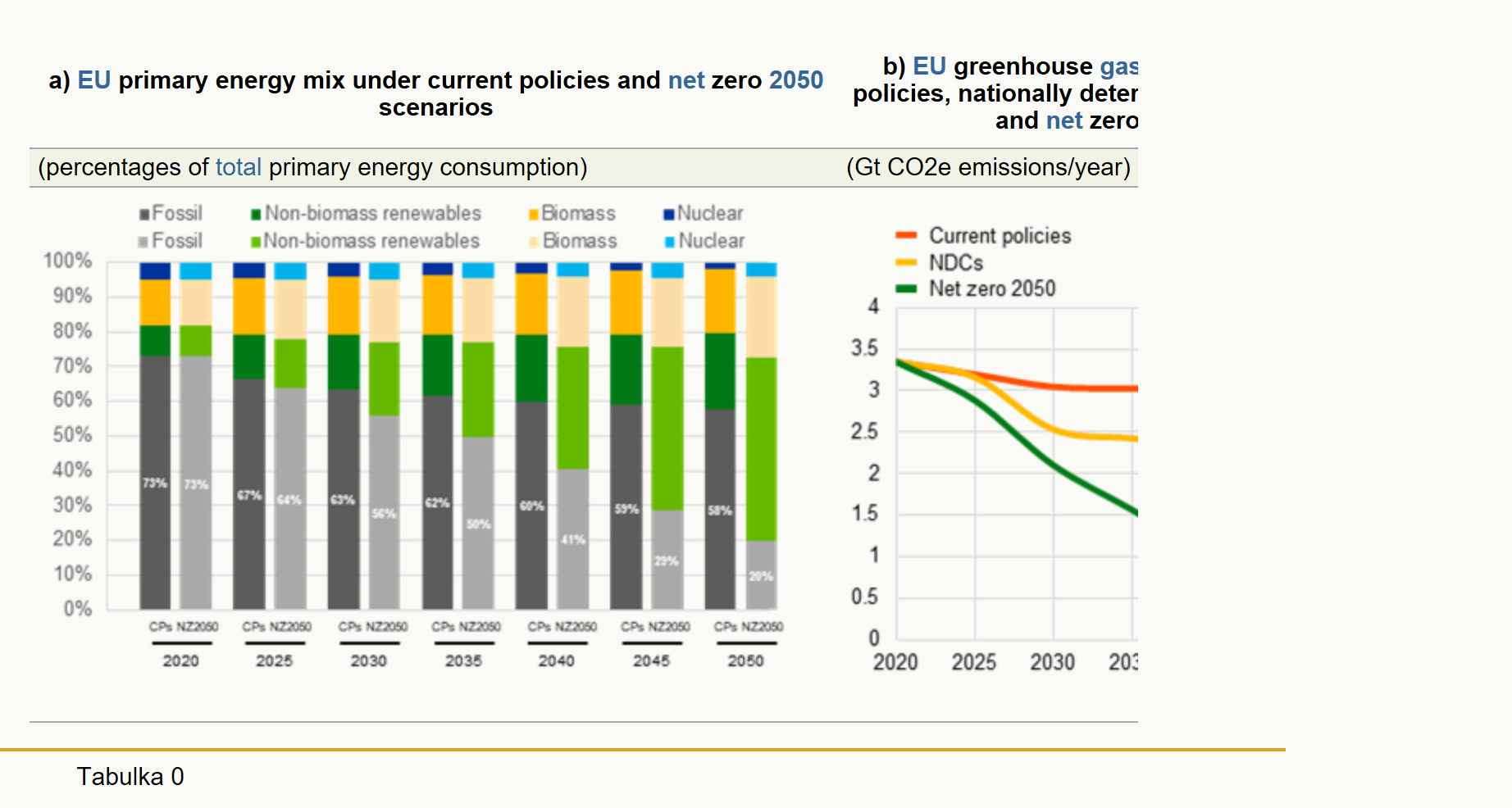

The Network for Greening the Financial System (NGFS), which brings together central banks and supervisors working on climate issues around the world, has developed scenarios to assess how economies might look on different climate policy paths. These scenarios underline that to achieve the net zero target by 2050 the share of fossil fuels in the EU energy mix must be reduced from around 73% in 2020 to around 20% in 2050, However, current policies would only reduce it to slightly below 60% (Chart 1, panel a). Under current policies, we would fall well short of the net zero target in 2050. Even if all existing national pledges were fulfilled, there would still be a large gap (Chart 1, panel b).[9]

Chart 1

EU primary energy mix and EU greenhouse gas emissions under different NGFS scenarios from 2020 until 2050

Source: NGFS. Data is derived from the GCAM 6.0 NGFS model covering the EU27.

Notes: Current policy scenario (CPs): assumes that only currently implemented policies are maintained, leading to high physical risks.

Nationally determined contributions scenario (NDCs): includes all pledged policies, even if not yet implemented, resulting in a moderate and heterogeneous climate goal that leads to a decline in CO2 emissions but only limits global heating to 2.6°C. Net zero 2050 (NZ2050) scenario: assumes that stringent climate policies are implemented and innovations take place, limiting global warming to 1.5°C, reaching net zero CO2 emissions by 2050.

To put the scale of action required into context, consider the investment required to meet the EU’s green transition objectives. The European Commission has estimated that additional investment of €620 billion a year will be needed between 2023 and 2030 (Chart 2).[10] This amounts to 3.7% of the EU’s 2023 GDP. In addition to this, the EU will also need to invest in climate resilience to prepare for the effects of climate change that can no longer be avoided.[11] Global temperatures are indeed on a trajectory that is far above the Paris Agreement goals.[12]

Chart 2

EU additional annual investment needs to meet the European Green Deal objectives, 2023-2030

(EUR billions per year and percentages)

Source: European Commission.

Notes: Average annual investment needs to meet the objectives set out under various EU initiatives related to the green transition in addition to historical investments (2011-2020).

We are therefore now at the next stage of the tragedy of the horizon. Since we did not invest enough in the past, when the impacts seemed far off, we are now confronted with higher costs in terms of both the impact climate change is having on our economy today and the investment required to mitigate future damage. And we are exposed to a vicious cycle, where the economy finds itself caught in a continuous loop of crisis management, which reduces the scope for making the necessary investments in the green transition.[13]

But we should make no mistake: delaying the transition would be more costly. Results from ECB economy-wide top-down stress test show that transition costs are lower than the long-term costs of unabated climate change.[14]

Implications for central banks

This situation has profound implications for central banks’ core task of preserving price stability.[15]

Let me mention a few of them.

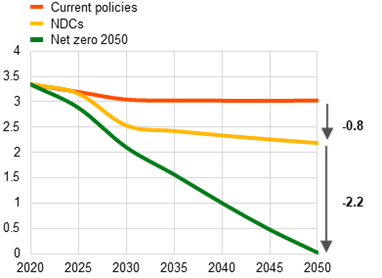

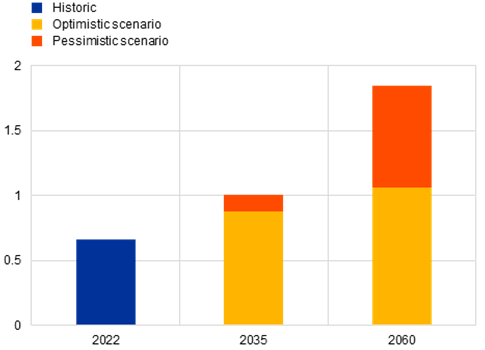

First, evidence underscores how extreme weather, such as unusually hot summers, affects both the level of inflation and its volatility. For example, ECB research estimates that the extreme summer heat in 2022 increased food inflation in Europe by around 0.7 percentage points cumulatively over 12 months. These effects could be even more pronounced in the future, increasing to 1% in 2035 and to almost 2% in 2060 (Chart 3).[16] More broadly, climate change could increase the frequency of supply side shocks, which are more difficult to deal with, take longer to be reabsorbed and result in high losses in income and employment, as they push inflation up and economic growth down.

Chart 3

Impact of heatwaves on food price inflation

(percentage points)

Sources: Kotz et al (2023).

Notes: Estimated with a global panel regression approach using monthly prices and high-resolution climate data. Cumulative deviation of food inflation from baseline after 12 months due to extreme temperatures from June to August are shown. The chart is based on combining elasticities of a 1°C increase in temperatures with results from 21 global climate models. Projected temperatures of a 2022-like summer (i.e. in the upper tail of the temperature distribution) in future climates are retrieved from climate model results under an optimistic (“below 2°C by 2100” according to Representative Concentration Pathway (RCP) 2.6) and a pessimistic (“hot house world” according to RCP8.5) emissions scenario. Impacts could be reduced through ambitious adaptation to warmer climates.

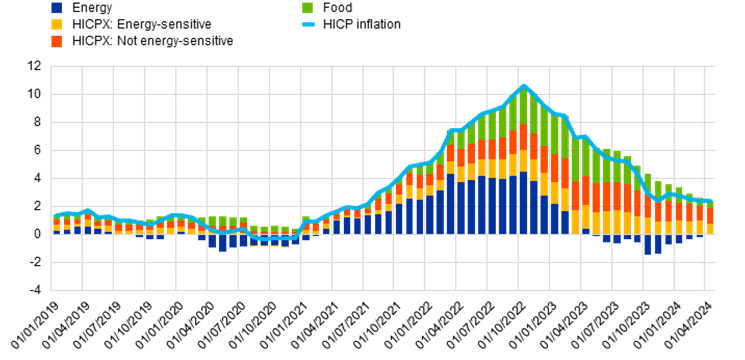

Second, a slow green transition increases the economic impact of these supply shocks. Europe paid a high price for its dependence on fossil fuels when Russia’s war of aggression in Ukraine triggered a sharp rise in energy prices and a spike in inflation. Taken together, the increase in prices of energy and energy-sensitive goods and services contributed around 6 percentage points to euro area inflation at its peak above 10% in October 2022 (Chart 4). Greater availability of renewable energy would have reduced the magnitude of the shock.[17]

Chart 4

Contribution of components of euro area headline HICP inflation

Source: Eurostat and ECB calculations.

Notes: HICP is the Harmonised Index of Consumer Prices (HICP). HICPX refers to HICP inflation excluding food and energy, and can be broken down into HICP non-energy industrial goods (NEIG) and HICP services. Items are classified into energy-sensitive and not energy-sensitive at sub-item level (COICOP5). An item within HICP NEIG and HICP services is classified as energy-sensitive if its energy input cost share is greater than the average energy input cost share for, respectively, HICP NEIG and services.[18] Last observation: April 2024.

Third, beyond inflation, climate change and extreme weather events can also affect the capital stock and labour productivity.[19] For instance, studies have found that a 1°C increase in temperatures above 25°C reduces productivity by roughly 2%.[20] Climate change constrains potential output and productivity growth, thereby reducing the level at which GDP growth and real wage gains may become inflationary. It may also be difficult to anticipate the impact on the natural rate of interest, i.e. the real rate of interest that is neither expansionary nor contractionary, making it more difficult to conduct monetary policy. Increasing climate-related damages and uncertainty may reduce productivity growth, raise precautionary savings and therefore dampen the natural rate of interest, whereas investment and innovation stemming from transition policies could affect it positively.[21]

Fourth, if not correctly priced in, climate change implies financial risks for the central bank’s balance sheet. An accurate valuation of these risks is therefore key to protect the ECB’s balance sheet.[22] Likewise, banks’ balance sheets face similar financial risks, which upon materialisation may impact their soundness and thus the monetary policy transmission mechanism.[23]

The role of the ECB

So what can the ECB do within its mandate?

Establishing the right framework conditions

The ECB’s monetary policy decisions are guided by our primary objective, which is to pursue price stability, defined as a target of 2% inflation over the medium term. Without prejudice to this primary objective, the ECB and national central banks support the general economic policies in the European Union with a view to helping to achieve its objectives. This includes supporting the green transition of the economy in line with the EU’s climate objectives. We have both our primary objective and our secondary objective in mind when it comes to dealing with climate change.

By pursuing price stability, we are contributing to a stable and predictable macroeconomic environment. This is essential to generate the resources and incentives required for long-term planning and investment in the green transition.

This means that we must take the necessary action when inflation is deviating from our medium-term target. And that’s exactly what the ECB has done since July 2022, helping to bring inflation rapidly down from its peak of 10.6% in October 2022 to 2.4% last month. Barring any further shocks, we expect inflation to fluctuate around current levels in the coming months before falling to our target next year. As supply shocks unwind, we can finally turn our attention to pursuing lower inflation and higher growth simultaneously. Recent data go in that direction and increase our confidence that we will be able to dial back our restrictive monetary policy stance. So although tighter financing conditions have temporarily increased the cost of borrowing, they have helped keep inflation expectations anchored, increased confidence that inflation will return to our target, and ultimately contributed to a lower cost of funding for long-term projects related to the green transition, which were also temporarily affected by higher borrowing costs.[24][25]

Price stability is crucial to helping us achieve net zero because it enables households and businesses to better detect relative price changes and to factor these into their decisions. As extensive changes in consumption patterns and production technologies are required to achieve the net zero scenario, price signals are critical when setting the right incentives for the green transition. For instance, the recent spike in energy prices contributed to a sustained reduction in energy consumption and the energy intensity of the European economy. The European Commission has estimated that demand for natural gas in the EU declined by 18% between August 2022 and March 2024, exceeding the 15% reduction target set after Russia’s invasion of Ukraine.

Looking ahead, a key question for monetary policy is how to address the risk of more frequent supply shocks, the effects of which are magnified by climate change and insufficient progress on the green transition. On the one hand, central banks could consider reacting more quickly to large shocks, both when they occur and when they unwind, to preserve an appropriate monetary policy stance. On the other hand, central banks should avoid excessively tightening financing conditions to pre-empt any potential inflationary effects caused by shocks that have not yet materialised. This approach could be counterproductive because it reduces potential output and investments that could enhance our resilience to such shocks.

Factoring climate change into our tasks

Beyond establishing the right framework conditions as part of our price stability mandate, we are factoring climate change into our tasks.

First, since the ECB strategy review of 2020-2021 we have been integrating climate considerations into our monetary policy framework.[26] In October 2022 we started tilting the reinvestments of our corporate bond holdings towards issuers with a better climate performance.[27] Moreover, climate-related financial risks are considered in regular reviews of collateral haircut schedules.[28] In 2023 we also started disclosing the climate impact of our corporate sector portfolio held for monetary and non-monetary policy purposes annually. We have committed to continuously improving our disclosures as the quality and availability of data improve, and to expanding the scope of these disclosures to our other monetary policy portfolios.[29]

Following the recent review of our operational framework, we decided to incorporate climate change-related considerations into our structural monetary policy operations.[30] Moreover, in the future we will only accept marketable assets and credit claims from companies and debtors that comply with the Corporate Sustainability Reporting Directive as collateral in Eurosystem credit operations. And we intend to limit the share of assets issued by firms with a high carbon footprint in the collateral pools of counterparties once the necessary technical preconditions are in place.[31]

Second, we are taking action as part of our responsibility for supervising banks. In particular, we have taken measures to ensure that banks manage climate-related and environmental risks. While banks have made progress on this in recent years[32], more works lies ahead[33]. Banks also remain susceptible to greenwashing[34] and they still lend disproportionately to sectors with high exposure to climate-related risk and to high-emitting households.[35]

Third, we are taking measures to reduce the environmental footprint of banknotes and payment systems. For example, for banknotes, we use only 100% sustainable cotton and banned the disposal of banknote waste in landfill.[36] In the field of payment systems, we are considering environmental aspects in the design of a digital euro.

Fourth, we are seeking to reduce our organisation’s environmental footprint. Since 2010 the ECB has run a certified environmental management system covering its own operations. In the last ten years we reduced electricity and heating consumption per workplace by 30% and 49% respectively. Taking emission reduction targets as a reference, in 2021 the ECB committed to reducing its own operations’ footprint by 46.2% by 2030, taking 2019 as a baseline.

Finally, we play a key role through our research and analysis. Beyond their direct relevance to our tasks, our findings may also be useful for other policy areas supporting the green transition. For example, we contribute actively to the work of the NGFS and provide advice on financial legislation as foreseen under the Treaties.

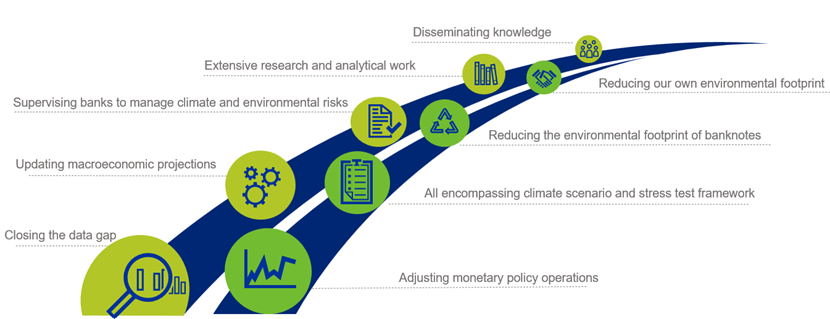

We recently took stock of the progress we have made so far (Chart 5). The ECB’s new climate and nature plan 2024-2025 sets out our renewed commitment to take action, within our mandate, to support the green transition.[37] We will continue to implement measures that we have already agreed upon in the fields of macroeconomic analysis, monetary policy, banking supervision, climate-related data and our own corporate sustainability. In addition, the plan sets out three focus areas for 2024-25: navigating the transition to a green economy, addressing the increasing physical impact of climate change and advancing work on nature loss and degradation. These focus areas will guide our exploratory and analytical work in the coming years.

Chart 5

The ECB has implemented several measures to incorporate climate change considerations into its activities

Source: ECB.

Complementarity with other policies

Notwithstanding these initiatives, it is important to emphasise that the primary responsibility for leading the green transition lies with elected governments, which possess more direct tools and the legislative power to enact the necessary changes. Since there are important complementarities between these policies and monetary policy, the ECB stands ready to offer support by providing technical analysis and advice. This knowledge sharing lies squarely within the scope of our primary mandate insofar as these other policies, by mitigating climate change risks, will allow monetary policy instruments to more effectively preserve price stability.

Let me provide some examples of these complementarities.

Addressing supply shocks

A first example is the complementarity with policies aimed at cushioning supply shocks.

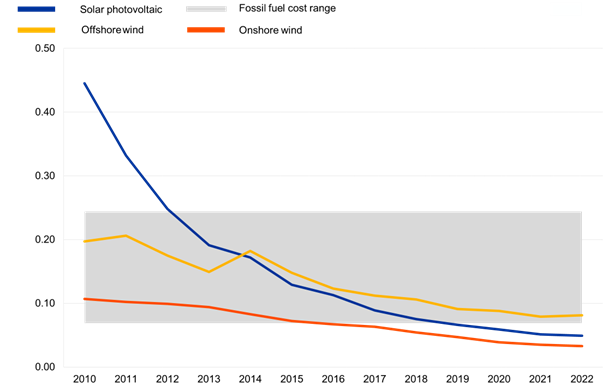

In particular, policies that support diversification away from fossil fuels and increase energy efficiency enhance the resilience of our economy to shocks stemming from energy commodities prices, thereby containing inflationary pressures. Remarkable technological advances in recent years have greatly enhanced the efficacy and reduced the cost of sustainable technologies. Notably, the period from 2010 to 2022 saw dramatic decreases in the cost of producing electricity from offshore wind, onshore wind and solar energy by 60%, 70% and 90% respectively (Chart 6).

Chart 6

Decrease in the cost of renewable sources of electricity between 2010 and 2022

Source: International Renewable Energy Agency (2023), “Renewable Power Generation Costs in 2022”, Abu Dhabi.

Note: The cost of renewable energy sources is based on data for 2022.

At the same time, efforts to secure the supply of key raw materials, jointly purchase them or support innovation to reduce dependency on them can help lessen our exposure to the price and availability of metals and minerals like copper or lithium that are critical for the green transition.

Likewise, measures to ease the impact on households and businesses of fossil fuel energy price spikes can be designed so as not to suppress the price signal, which is key for providing incentives to reduce consumption of and dependency on fossil fuels.[38]

Mitigating the negative impact of climate change on productivity and potential output

Second, other policies can mitigate the negative impact of climate change on productivity and potential output.

The EU’s Emissions Trading System (ETS) is a key policy tool for supporting the green transition by effectively incentivising the private sector to adopt cleaner technologies and processes. This policy has not only contributed to a reduction in emissions but has also spurred innovation in green technologies.[39]

Policies that support innovation and the deployment of renewable energy technologies can also yield high returns. Notably, advancements in renewable energy sources, battery storage and smart grids are possibly reaching a tipping point: as these solutions become more widely adopted and developed, they encourage further deployment, creating a self-reinforcing cycle of innovation and investment.[40] In this respect, it is worth recalling that the integration of the European energy market – by creating a genuine energy union – would allow us to reap benefits in terms of scale and diversification, leading to both increased efficiency and greater resilience.

This also matters for Europe’s competitiveness. As with digitalisation, the ability to offer the world-leading technologies, products and services needed for the green transition will decide tomorrow’s winners and losers in the global productivity race.

Mobilising funding to cover investment needs

Third, let me emphasise the complementarity with macroeconomic policies that have the potential to generate useful resources for the green transition and to mobilise them effectively for this purpose.

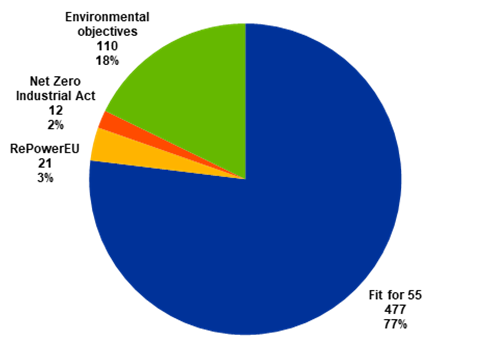

The EU already dedicates a large share of its funding to green objectives. According to the European Commission, a total of €578 billion will be allocated to supporting climate action over the current budgetary period from 2021 to 2027, around 33.5% of the overall portfolio. The instrument set to make the largest contribution is the Recovery and Resilience Facility (RRF), which accounts for 35% of the overall climate action budget (Chart 7). But the RRF is a temporary tool. Once it is discontinued in 2026, the EU budget for the green transition will shrink significantly as a result of the cliff effect.[41]

Chart 7

Commitments under the European Commission’s Multiannual Financial Framework 2021-2027 and Next Generation EU that contribute to climate mainstreaming, as a share of the EU’s total green budget, by programme

(€ billions and percentages)

Sources: European Commission Programme Performance Statements and ECB calculations.

Further efforts to mobilise fiscal resources at EU level may include some reprioritisation of the EU budget, an increase in the EU’s own resources, as well as the promotion of new joint debt issuance initiatives to fund investment in genuine European public goods – for instance energy grids and interconnections. We can and should learn from our experiences with existing instruments to design effective tools.[42]

But the bulk of the funding for the transition will have to come from private funding sources. In the euro area, banks will play an essential role in supporting investment and the adoption of green technologies by firms and households. However, a key EU policy objective is to further develop capital markets[43], which could provide specialised funding and support innovation.[44]

The market for green financial products has grown significantly in recent years,[45] but there is room for more progress. In a recent report on the future of the Single Market, Enrico Letta pointed to the need to better channel private savings into the green transition. He noted that there are approximately €33 trillion in private savings sitting in current accounts in the EU, which are therefore not being fully leveraged to meet investment needs.[46]

Better channelling these private funds could provide a substantial boost to the EU’s green investment goals. To achieve this, it is essential to make further progress on completing the capital markets union. In this respect, the EU could also explore the scope for measures that target green segments of capital markets.

Conclusion

In conclusion, the urgent need to combat climate change cannot be overstated. We should have acted yesterday, and we certainly cannot afford to wait until tomorrow.

Climate change is accelerating as we speak and it has important implications for central banks because it has an impact on inflation and the exposure to supply shocks, while lowering potential output and productivity growth. It also creates financial risks for the central bank’s balance sheet.

So we face two mutually exclusive paths: either we choose inaction and find ourselves trapped in a vicious cycle of constantly responding to escalating crises or we proactively seek to prevent the emergence of new climate and energy crises through sound and coordinated policies.

At the ECB, we are steadfast in our commitment to support the green transition within the scope of our mandate. However, this is not a task we can accomplish alone. It requires a collective effort by all stakeholders across Europe. In turn, we as central banks can benefit from these efforts in the pursuit of our objectives.

Specifically, the EU will need to implement robust supply side policies to move away from fossil fuels, enhance energy efficiency and ensure the availability of key raw materials. To transform our ambitions into tangible outcomes, substantial investments are necessary. By pooling resources across Europe and establishing a strong capital markets union, we can attract significant private capital – and direct it towards sustainable projects.

The path ahead is challenging, but Europe has a proven track record of rising to the occasion when it matters most.

Thank you.

-

Carney, M. (2015), “Breaking the Tragedy of the Horizon – climate change and financial stability”, speech at Lloyd’s of London, September.

-

According to the World Meteorological Organization’s latest report, 2023 was the hottest year on record by a clear margin, with the global mean near-surface temperature at 1.45 °C above the pre-industrial average.

-

World Meteorological Organization (2024), “State of the Global Climate 2023”, March.

-

Copernicus Climate Change Service and World Meteorological Organisation (2024), “European State of the Climate report 2023”, April.

-

European Environment Agency (2023), “Economic losses from weather and climate related extremes in Europe”, October.

-

ECB-EIOPA (2023), “Policy options to reduce the climate insurance protection gap”, Discussion Paper, April.

-

EIOPA (2023), “Measures to address demand side aspects of the natcat protection gap”, Staff paper, July.

-

For example, in December 2023 the European Commission’s assessment found that the measures in Member States’ draft National Energy and Climate Plans (NECPs) were insufficient to achieve the EU’s 2030 targets for greenhouse gas emissions, carbon removals, renewable energy and energy efficiency (press release). In January 2024 the European Scientific Advisory Board on Climate Change found that more efforts were needed across all sectors to achieve the EU’s climate objectives from 2030 to 2050, particularly in buildings, transport, agriculture and forestry (press release).

-

Data is available here. The figures refer to the GCAM 6.0 NGFS scenario.

-

These investment needs come in addition to the historical investment, which for climate-related investment only amounted to €477 billion per year for the decade 2011-2020.

-

There is a very wide range of estimates for these needs, spanning from €35 billion to €500 billion per year. See European Investment Bank (2021), “The EIB Climate Adaptation Plan. Supporting the EU Adaptation Strategy to build resilience to climate change”.

-

See United Nations Environment Programme (2023), Emissions Gap Report 2023: Broken Record – Temperatures hit new highs, yet world fails to cut emissions (again); and F. Elderson (2024), “’Know thyself’ – avoiding policy mistakes in light of the prevailing climate science”, keynote speech at the Delphi Economic Forum IX, 12 April.

-

In response to the recent energy crisis, driven by a surge in the price of fossil fuels, governments had to allocate nearly 2% of GDP in 2022 and 2023 to cushion the shock.

-

See Emambakhsh, T. et al. (2023), “The Road to Paris: stress testing the transition towards a net-zero economy”, Occasional Paper Series, No 328, ECB, September.

-

See also Lagarde, C. (2021), “Climate change and central banking”, keynote speech at the ILF conference on Green Banking and Green Central Banking, 25 January, and Work stream on climate change (2021), “Climate change and monetary policy in the euro area”, Occasional Paper Series, No 271, ECB, September.

-

See “The price of inaction: what a hotter climate means for monetary policy”, The ECB Blog, December 2023.

-

To cushion the impact of the electricity price spike, the EU imposed a temporary revenue cap on producers with lower marginal costs, such as renewable energy producers. See Panetta, F. (2022), “Greener and cheaper: could the transition away from fossil fuels generate a divine coincidence?”, speech at the Italian Banking Association, 16 November.

-

For details, Fagandini, B., Goncalves, E., Rubene, I., Kouvavas, O., Bodnar, K. and Koester, G. (2024), “Decomposing HICPX inflation into energy-sensitive and wage-sensitive items”, Economic Bulletin, Issue 3, ECB, 2024.

-

See Parker, M. (2023), “How climate change affects potential output”, Economic Bulletin, Issue 6, ECB, 2023; Bijnens et al. (2024), “The impact of climate change and policies on productivity,” Occasional Paper Series, No 340, ECB.

-

Heal, G. and Park, J. (2016), “Reflections—temperature stress and the direct impact of climate change: a review of an emerging literature”, Review of Environmental Economics and Policy, Vol.10, No 2, University of Chicago Press.

-

See Mongelli, F. P., Pointner, W. and van den End, J. W. (2022), “The effects of climate change on the natural rate of interest: a critical survey”, Working Paper Series, No 2744, ECB.

-

Panetta, F. (2021), “Sustainable finance: transforming finance to finance the transformation”, speech at the 50th anniversary of the Associazione Italiana per l’Analisi Finanziaria, 25 January.

-

See F. Elderson (2023), “Monetary policy in the climate and nature crises: preserving a ‘Stabilitätskultur’”, speech at the Bertelsmann Stiftung, 22 November.

-

Recent analysis has shown that, while restrictive monetary policy generally tightens financing conditions and slows investment for all firms – including investments aimed at reducing carbon emissions – monetary policy tightening does not tend to imply a worsening in lending conditions for green firms relative to non-green firms. See Altavilla, C. et al (2023), “Climate Risk, Bank Lending and Monetary Policy”, Discussion Paper, No 18541, CEPR, 20 October.

-

The ECB’s Survey on the Access to Finance of Enterprises (SAFE) confirms that more than half of firms in the euro area see high interest rates as an impediment to future investment in the green transition. For further information on the answers to the ad-hoc questions on green investment and financing in the SAFE, please see Ferrando, A., Groß, J. and Rariga, J. (2023), “Climate change and euro area firms’ green investment and financing ? results from the SAFE”, Economic Bulletin, Issue 6, ECB, 2023.

-

See “ECB presents action plan to include climate change considerations in its monetary policy strategy”, press release, ECB, 8 July 2021.

-

The tilting was strengthened when partial reinvestment of maturing securities started in March 2023. See “Monetary policy decisions”, press release, ECB, 2 February 2023.

-

See “ECB reviews its risk control framework for credit operations”, press release, ECB, 20 December 2022. These schedules were found to be sufficiently protective against climate-related financial risks in the latest review in December 2022.

-

Such as those under the public sector purchase programme (PSPP), the third covered bond purchase programme (CBPP3) and other assets under the PEPP. See “ECB starts disclosing climate impact of portfolios on road to Paris-alignment”, press release, ECB, 23 March 2023.

-

Specifically, whenever the ECB is faced with two configurations of instruments that would be equally conducive to maintaining price stability, it shall choose the one that best supports the general economic policies in the EU. This implies that whenever it adjusts the calibration of our instruments, it must choose the option that increases confidence in the plausibility of its decarbonisation path, unless a proportionality assessment shows that there are other, less intrusive ways of achieving price stability. See ECB, “Changes to the operational framework for implementing monetary policy”, Statement by the Governing Council, 13 March 2024.

-

See “ECB takes further steps to incorporate climate change into its monetary policy operations”, press release, ECB, 4 July 2022.

-

See Altavilla C., Boucinha M., Pagano M., Polo A. (2023), “Climate risk, bank lending and monetary policy”, CEPR Discussion Paper No. 18541.

-

For example, banks’ materiality assessments and business environment scans are becoming more robust compared with their initial submissions. Furthermore, the banks that did not perform an adequate materiality assessment received binding supervisory decisions, including the potential imposition of periodic penalty payments if they fail on their requirements. See Elderson, F. (2024), “Making banks resilient to climate and environmental risks – good practices to overcome the remaining stumbling blocks”, speech at the 331st European Banking Federation Executive Committee meeting, 14 March; and Elderson, F. (2024), “You have to know your risks to manage them – banks’ materiality assessments as a crucial precondition for managing climate and environmental risks”, The Supervision Blog, 8 May.

-

See Giannetti, M., Jasova, M., Loumioti, M., and Mendicino, C. (2023), "Green lending: do banks walk the talk?”, The ECB Blog, 6 December; and Giannetti, M., Jasova, M., Loumioti, M., and Mendicino, C. (2023), “‘Glossy Green’ Banks: The Disconnect Between Environmental Disclosures and Lending Activities”, Working Paper Series, No 2882, ECB.

-

See ECB/ESRB (2023), “Towards macroprudential frameworks for managing climate risk”, December 2023.

-

See the Eurosystem’s “Product Environmental Footprint study of euro banknotes as a payment instrument”, December 2023.

-

ECB, “Climate and nature plan 2024-2025”, January 2024.

-

For instance, horizontal tax breaks can be used to both compensate for lost income and smooth the spike in overall inflation.

-

See Känzig, D. (2023), “The unequal economic consequences of carbon pricing”, NBER Working Papers, No 31221, National Bureau of Economic Research, May and Hengge et al. (2023), “Carbon policy surprises and stock returns: Signals from financial markets”, IMF Working Papers , No 2023/013, 27 January.

-

See “The Breakthrough Effect: How to trigger a cascade of tipping points to accelerate the net zero transition”, SYSTEMIQ, January 2023.

-

The Social Climate Fund will become operational in 2026 and will partially compensate for the end of the RRF programme by providing up to €65 billion over the period 2026-2032 to support structural measures and investments in energy efficiency and renovation of buildings, clean heating and cooling, and integration of renewable energy, as well as in zero and low-emission mobility solutions.

-

For more information on proposals to enhance EU financing for the green transition, see Abraham, L., O'Connell, M., L. and Arruga Oleaga, I. (2023), “The legal and institutional feasibility of an EU Climate and Energy Security Fund”, Occasional Paper Series, No 313, ECB, 2023; Arnold, M. N. G., Balakrishnan, M. R., Barkbu, M. B. B., Davoodi, M. H. R., Lagerborg, A., Lam, M. W. R. et al. (2022), “Reforming the EU fiscal framework: Strengthening the fiscal rules and institutions”, IMF Working Paper, No 2022/014, 5 September; Monasterolo, I., Pagano, M., Pacelli, A. and Russo, C. (2024), “A European Climate Bond”, available at SSRN, March.

-

See European Council (2024), “Special meeting of the European Council (17-18 April 2024) - Conclusions”; ECB (2024), “Statement by the ECB Governing Council on advancing the Capital Markets Union”, 7 March; Lagarde, C. (2023), “A Kantian shift for the capital markets union”, speech at the European Banking Congress, Frankfurt am Main, 17 November; and Panetta, F. (2023), “Europe needs to think bigger to build its capital markets union”, The ECB Blog, 30 August.

-

Research by ECB staff suggests that carbon-intensive industries reduce emissions faster in economies with deeper stock markets because they facilitate green innovation, resulting in lower carbon emissions per unit of output. See De Haas, R., Popov, A. (2023), “Finance and Green Growth”, The Economic Journal, Vol. 133, Issue 650, February, pp. 637-668.

-

According to the ECB’s new experimental indicators on climate finance, the value of the market for sustainable debt securities in the euro area has increased steadily from around €450 billion at the beginning of 2021 to almost €1,500 billion today. However, this still only accounts for 6.6% of all debt securities issuance.

-

Letta, E. (2024), “Much More Than a Market: Speed, Security, Solidarity – Empowering the Single Market to deliver a sustainable future and prosperity for all EU Citizens”, Institut Jacques Delors, France, 27 April.

Related topics

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts

{kind=link}