Bank of Russia tightens restrictions on lending to highly indebted borrowers (24.11.2023)

The Bank of Russia has established new macroprudential limits on unsecured consumer loans for 2024 Q1. The decision has been made to limit the over-indebtedness of households and specifically of those with high debt-service-to-income ratios.

In making this decision, the Bank of Russia Board of Directors was guided by the following.

Macroprudential limits (MPLs) made it possible to reduce the share of new loans issued to borrowers with high DSTI ratios. The share of new loans issued by banks to borrowers with DSTI ratios1 exceeding 80% decreased from 36% in 2022 Q4 (before the introduction of the MPLs) to 25%2 in 2023 Q3 (from 41% to 25% for loans issued by microfinance organisations (MFOs). Over the same period, the share of bank loans with DSTI ratios from 50% to 80% was up from 27% to 33% (for MFOs, from 17% to 20%). Therefore, the Bank of Russia has also set MPLs on the share of loans with DSTI ratios from 50% to 80% with effect from 2023 Q4.

In October this year, as the regulator tightened its monetary and macroprudential policies, growth in outstanding amounts on unsecured and consumer loans slowed down to 1.1%3 (vs 1.5% in September and 2.4% in August). Growth in outstanding amounts varies significantly across the banking sector: the highest growth rates are observed among banks focusing on issuing credit cards, as the MPLs influence them with a lag. In this segment, a considerable part of funds (82%) is provided on credit cards issued before the introduction of the MPLs. That is why the Bank of Russia finds it reasonable to speed up the transition to a more balanced structure of credit card lending and has tightened the MPLs on such loans for 2024 Q1. On other loans, the limit has been also tightened, though to a lesser extent.

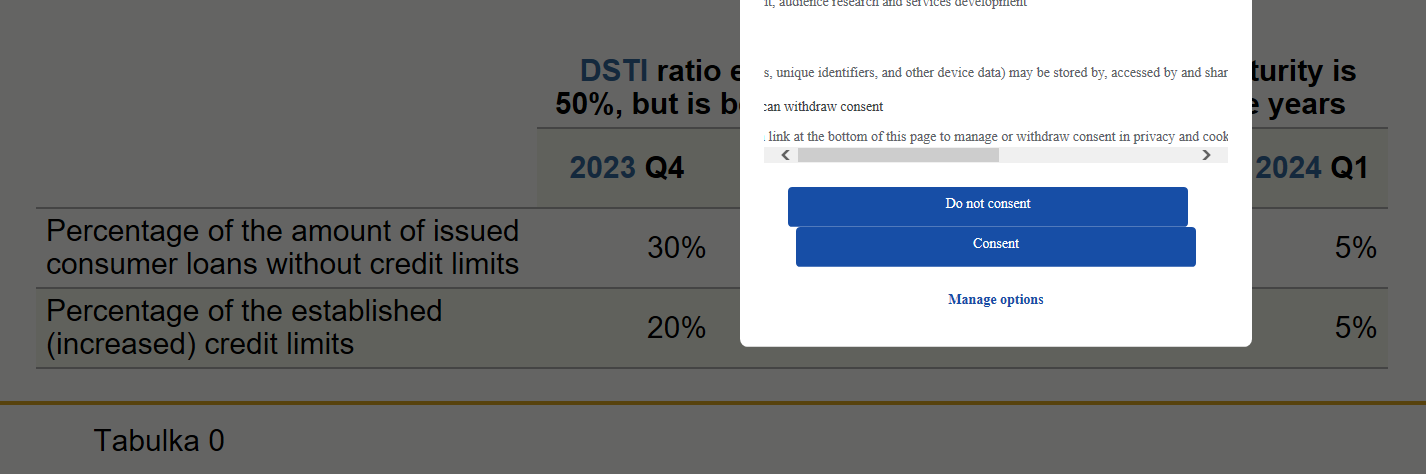

MPL values for banks (excluding banks with a basic licence):

| DSTI ratio exceeds 50%, but is below 80% | DSTI exceeds 80% | Loan maturity is over five years | ||||

|---|---|---|---|---|---|---|

| 2023 Q4 | 2024 Q1 | 2023 Q4 | 2024 Q1 | 2023 Q4 | 2024 Q1 | |

| Percentage of the amount of issued consumer loans without credit limits | 30% | 25% | 5% | 5% | 5% | 5% |

| Percentage of the established (increased) credit limits | 20% | 10% | 5% | 5% | 5% | 5% |

MPL values for MFOs:

| DSTI ratio exceeds 50%, but is below 80% | DSTI exceeds 80% | Loans maturity is over five years | ||||

|---|---|---|---|---|---|---|

| 2023 Q4 | 2024 Q1 | 2023 Q4 | 2024 Q1 | 2023 Q4 | 2024 Q1 | |

| Percentage of the amount of issued consumer loans without credit limits | 30% | 25% | 15% | 15% | No limit | |

| Percentage of the established (increased) credit limits | 20% | 15% | 15% | 15% | No limit | |

Since the introduction of the MPLs, the share of outstanding amounts on loans with DSTI exceeding 80% in banks’ portfolios has declined from 34% to 31%, though remaining high. Taking into account the MPL tightening in 2024 Q1, this share is expected to drop to 20%4 at the end of 2024. The MPL tightening will accelerate the transition to the balanced structure of outstanding consumer loans, which will ultimately mitigate risks for households, banks, and MFOs.

The Bank of Russia will make a decision on the parameters of macroprudential limits for 2024 Q2 in February 2024 considering changes in households’ debt burden and lending standards.

1 DSTI is the debt service-to-income ratio of a borrower. It is calculated as a ratio of borrower’s average monthly payments under all loans raised to the borrower’s average monthly income.

2 According to Reporting Form 0409704.

3 According to Reporting Form 0409115.

4 Unsecured consumer lending is assumed to expand in accordance with the growth rates set forth in the medium-term forecast approved by the Bank of Russia Board of Directors on 27 October 2023.

{kind=link}

{kind=link}